SK Hynix to Buy Intel’s NAND Memory Business For $9 Billion

by Ryan Smith on October 20, 2020 9:30 AM EST

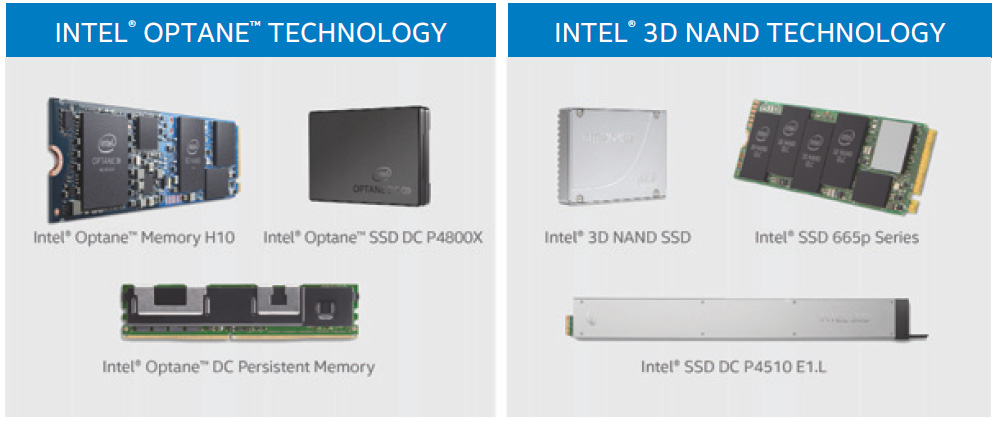

In a joint press release issued early this morning, SK Hynix and Intel have announced that Intel will be selling the entirety of its NAND memory business to SK Hynix. The deal, which values Intel’s NAND holdings at $9 billion, will see the company transfer over the NAND business in two parts, with SK Hynix eventually acquiring all IP, facilities, and personnel related to Intel’s NAND efforts. Notably, however, Intel is not selling their overarching Non-Volatile Memory Solutions Group; instead the company will be holding on to their Optane memory technology as they continue to develop and sell that technology.

Per the terms of the unusual agreement, SK Hynix will be acquiring Intel’s NAND memory business in two parts, with the deal not expected to completely close until March of 2025. Under the first phase, which will take place in 2021 once all relevant regulatory bodies have approved the seal, SK Hynix will pay Intel the first $7 billion for their SSD business and Intel’s sole NAND fab in Dalian, China. This will see Intel’s consumer and enterprise SSD businesses transferred to SK Hynix, along with the relevant IP and employees for the SSD business, but not any NAND IP or employees. Similarly, while SK Hynix will get the Dalian fab, the first phase does not come with the employees that operate it.

Following the first phase, Intel will continue to develop and manufacture NAND out of the Dalian fab for roughly the next four years. This period is set to last until the rest of the deal fully closes in March of 2025. At that point, SK Hynix will pay Intel $2 billion for the rest of their NAND business. This will finally transfer all of Intel’s NAND IP and related employees over to SK Hynix, along with the Dalian fab employees. Intel and SK Hynix have not offered any explanation for the prolonged acquisition, so we’re hoping to find out a bit more with the companies’ relevant earnings calls this week.

Meanwhile, Intel will continue to hold on to their Optane memory business. Optane is considered a “platform differentiator” by the company, as Intel intends to continue leveraging the technology for their unique, high-capacity NV-DIMMs. Accordingly, Intel has announced that they will be continuing to develop the underlying 3D XPoint technology and sell products based on it, which is consistent with their long-term aspirations of making Optane its own tier in the memory/storage hierarchy.

Overall, selling off their NAND business is a big step for Intel, a company that started out making memory. But it’s not entirely unexpected, as Intel has never been quite as successful with their NAND business as they would have liked. And the core of the company’s NAND efforts, their longstanding IMFT joint-venture with Micron, started winding down in 2018 when the two companies announced that they would stop jointly developing flash memory.

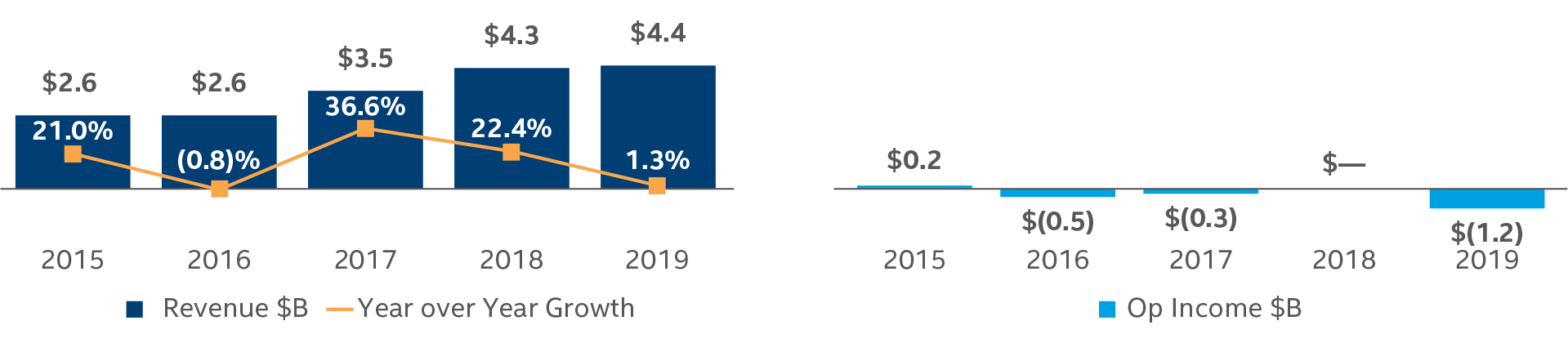

Since then, Intel has largely been walking its own path, securing the #5 spot in the NAND industry (generally right behind #4 SK Hynix) and releasing new products, but struggling with the commodity nature of the NAND business. While Intel’s Non-Volatile Memory Solutions Group (NSG) as a whole brought in $4.4B in revenue for 2019, the group has lost money for 4 of the last 5 years, recording flat or negative operating incomes. Only in the last six months has Intel made any real money off of NAND, reporting $600M in operating income for the first half of 2020. So although NSG – and by large part, Intel’s NAND business – have played a big part in Intel’s record revenues, they haven’t turned a significant profit for a company that’s renowned for their 60% gross margins.

Intel NSG Revenue and Operating Income, 2015-2019

Meanwhile for SK Hynix, the Intel deal opens the door to some new opportunities, and it also helps formerly fourth-place company company scale up to deal with the competition of its three remaining rivals, Samsung, Kioxia/WD, and Micron. TrendForce estimates that once this deal closes, SK Hynix will become the second-largest vendor of NAND, with over 20% market share, placing it behind market leader (and rival Korean firm) Samsung. Like many other commodity component markets, the NAND flash market has been subject to wild swings in profitability and the resulting pressure to consolidate, so by picking up Intel’s NAND business, SK Hynix will be in a stronger position going forward.

But the real pearl for SK Hynix is Intel’s enterprise SSD business, which the company specifically calls out in its joint press release. Despite its overall modest size, Intel’s NAND business has a major presence in the enterprise SSD market thanks to its early investment there as well as its domination of enterprise CPU sales. Intel’s chief (and arguably only serious) competitor in this space has been Samsung, so acquiring Intel’s SSD business makes SK Hynix that much more capable of going toe-to-toe with their biggest rival.

Intel Enterprise "Ruler" SSDs

Long term, however, it remains to be seen what SK Hynix will do with the NAND fab side of Intel’s business. While it’s clear that they have big plans for SSDs and intend to leverage Intel’s existing market share and customer relationships – which is a big part of why they’re acquiring that segment first – SK Hynix doesn’t necessarily need Intel’s NAND manufacturing technology. SK Hynix is plenty capable of building more fabs on its own if it wanted more raw NAND capacity, and indeed the company has undergone several expansions. Meanwhile the companies’ technologies are significantly different, as Intel relies on floating gate tech while SK Hynix uses charge trap tech. So although the two technologies have their trade-offs, it’s very questionable whether SK Hynix wants to continue developing both over the long run.

And for both parties, the long run really is the key. NAND flash is still facing a likely dead-end in the long run, as NAND has been scaled down almost as small as it can go before leakage becomes a serious problem. 3D NAND stacking has given NAND a second wind in the interim, but there’s only so far that can go, especially in respect to reducing bit costs. Which is a big part of the reason why Intel developed 3D XPoint to begin with, as the technology doesn’t suffer the same scalability restrictions. So although Intel is getting out of the NAND game, they are still very much in the storage game over the long run, now focused on a non-volatile memory technology that is expected to scale much further in the future.

Speaking of the future, Intel has also stated that they will be investing the expected proceeds from the sale into some of their other non-core, forward-looking businesses. Intel’s 5G, AI, and edge efforts are all slated to benefit from the sale, and all are markets that Intel is priming for potentially extreme growth over the coming years.

In the interim, however, the next step will be up to regulators. SK Hynix’s acquisition will need the approval of American, South Korean, and Chinese regulators, which the companies expect to take around a year – and at which point SK Hynix can start the actual acquisition. Meanwhile Intel is set to announce its Q3 earnings this Thursday, at which point we may hear a bit more about the deal from Intel’s perspective. SK Hynix’s own earnings call will follow in a couple of weeks, on November 3rd.

Source: SK Hynix & Intel

64 Comments

View All Comments

Kallan007 - Tuesday, October 20, 2020 - link

Ok, I stand corrected! My bad.lmcd - Tuesday, October 20, 2020 - link

Yea lol the SK is South Korea, and the article mentions how they rival Samsung within the region.Spunjji - Wednesday, October 21, 2020 - link

Even if they were Chinese, the post wouldn't make sense. Nobody's obliged to sell their company to China.Roy2002 - Tuesday, October 20, 2020 - link

What? China? And why this is an example? For what? What you are complaining even if Hynix is a Chinese company? What's your point???name99 - Tuesday, October 20, 2020 - link

The whole thing looks like financial engineering (Intel's new core competence, as opposed to real engineering).Robert Cringely, back when he was relevant, mid to late 90s (and Microsoft was king) used to refer to this quote from Frank Gaudette, MS CFO:

"Watch for any changes in our accounting,” said Gaudette. “If I need to I can start, depreciating the software and maintain earnings growth for years on flat revenue. Watch for the accounting changes, wait for the next uptick in the stock price, and then sell."

Well, the accounting changes came, and the changes in MS' status came with them.

Real engineering benefits all of humanity.

Financial engineering benefits whoever gets the bonuses, and the shareholders who are best at navigating the highs and lows....

Cullinaire - Tuesday, October 20, 2020 - link

Sad but true, at the end of the day public corporations are all vulnerable to this type of rot. All it takes is a weak succession and the vultures swoop in.Meteor2 - Wednesday, October 21, 2020 - link

Yeah because Microsoft is doing just *terribly*, 25 years laterSpunjji - Wednesday, October 21, 2020 - link

You might have skipped over a few significant developments in that 25 year period. They switched back to actually trying to innovate and pursuing new markets again (e.g. cloud services, games consoles).Spunjji - Wednesday, October 21, 2020 - link

Agreed. They'll magically show an increase in margins from doing this, which will help to offset the massive hits they're about to take in desktop and servers (they still seem to have a lock on notebooks and convertibles thanks to OEMs and Nvidia, we'll see how long that lasts).Zizy - Tuesday, October 20, 2020 - link

Eh, even if NAND stops scaling, this doesn't mean cost won't decrease. Take a look at the solar cells for example, great price per Wp wasn't due to efficiency improvement but due to incredible cost reduction. The same can happen for nand and keep it relevant for ages. Yes, it WILL hit physical wall eventually like every other tech, but I don't think it is going the way of dodo any time soon. Especially as no competing technology has better perf/$ yet.