Intel Reports Q3 2022 Earnings: Back To Profitability, But Still Painful

by Ryan Smith on October 27, 2022 6:00 PM EST- Posted in

- CPUs

- Intel

- Financial Results

While always an interesting topic by default, corporate earnings reports in the tech industry have become especially important in the last few months, as the industry prepares to weather what’s expected to be the biggest downturn in demand in the last several years. Intel’s brutal Q2’22 report, which found the company losing money on a GAAP basis for the first time in 5 years, seems to have been a herald of things to come for the largest industry, with AMD and other companies since issuing earnings warnings ahead of their own Q3 reports. So as the first major tech company to publish their complete Q3’22 earnings report, Intel is once again likely to be a barometer of the tech industry’s performance over the past three months.

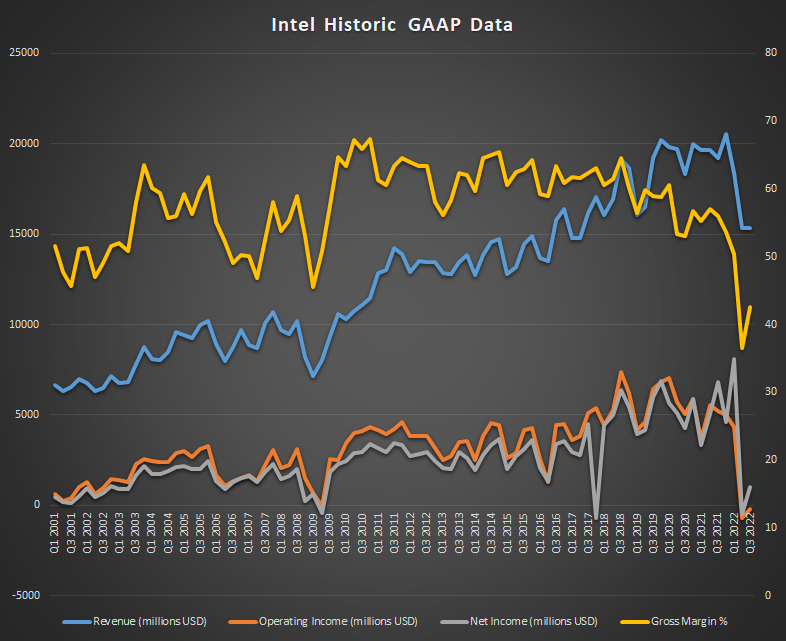

For the third quarter of 2022, Intel reported $15.3B in revenue, a $3.9B decline versus the year-ago quarter. Compared to Intel’s harsh Q2 report, the company has returned to profitability, booking a cool billion dollars in net income, though this is still well below their historical norms. In fact, the company is still operating at a (GAAP) loss, booking an operating income of -$175M. For Q3 at least, it would appear that it’s Intel’s tax situation that’s pushing them into the black, with the company recording a $1.2B tax benefit.

| Intel Q3 2022 Financial Results (GAAP) | |||||

| Q3'2022 | Q2'2022 | Q3'2021 | |||

| Revenue | $15.3B | $15.3B | $19.2B | ||

| Operating Income | -$175M | -$700M | $5.2B | ||

| Net Income | $1.0B | -$454M | $6.8B | ||

| Gross Margin | 42.6% | 36.5% | 56.0% | ||

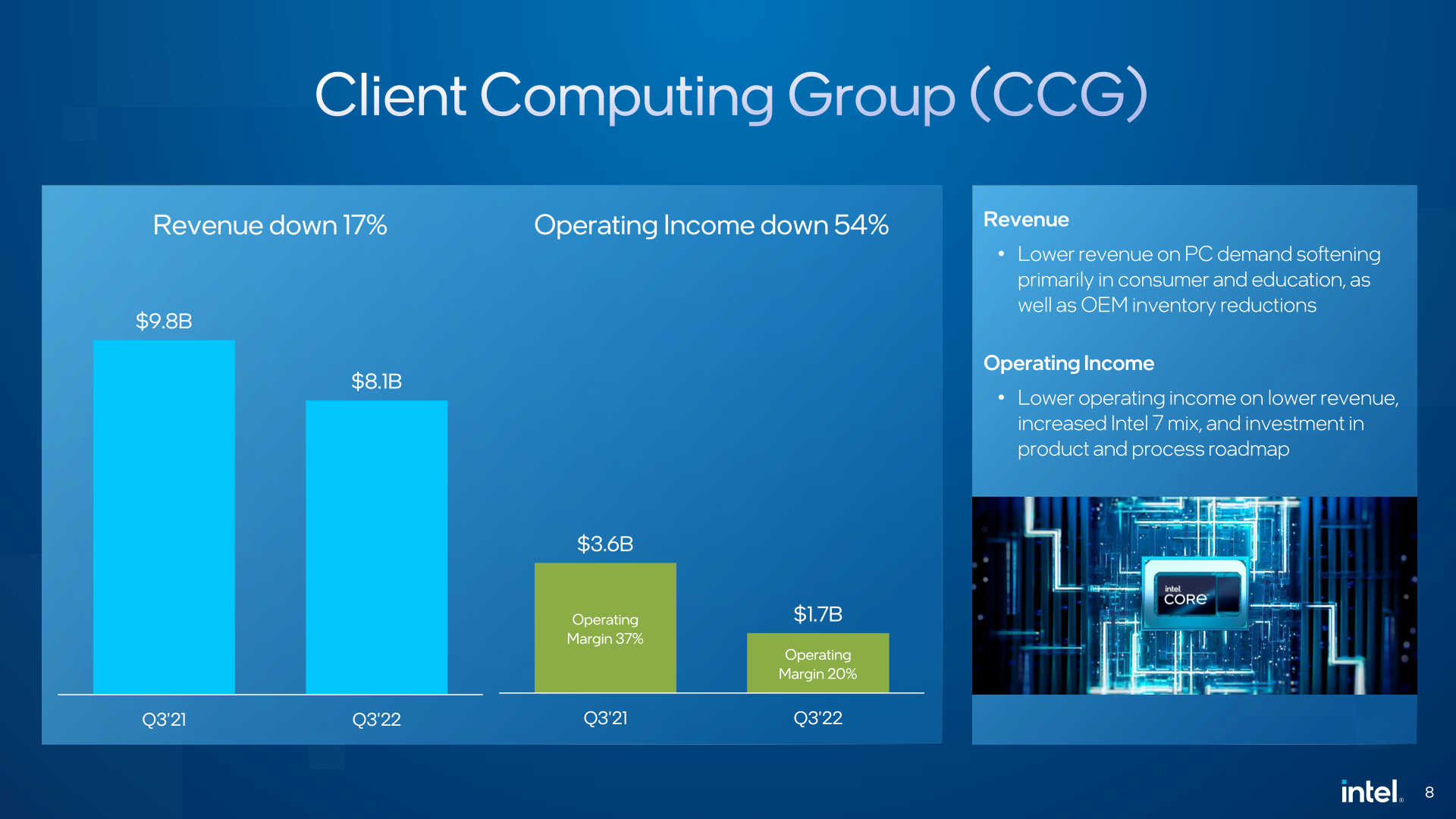

| Client Computing Group Revenue | $8.1B | +5% | -17% | ||

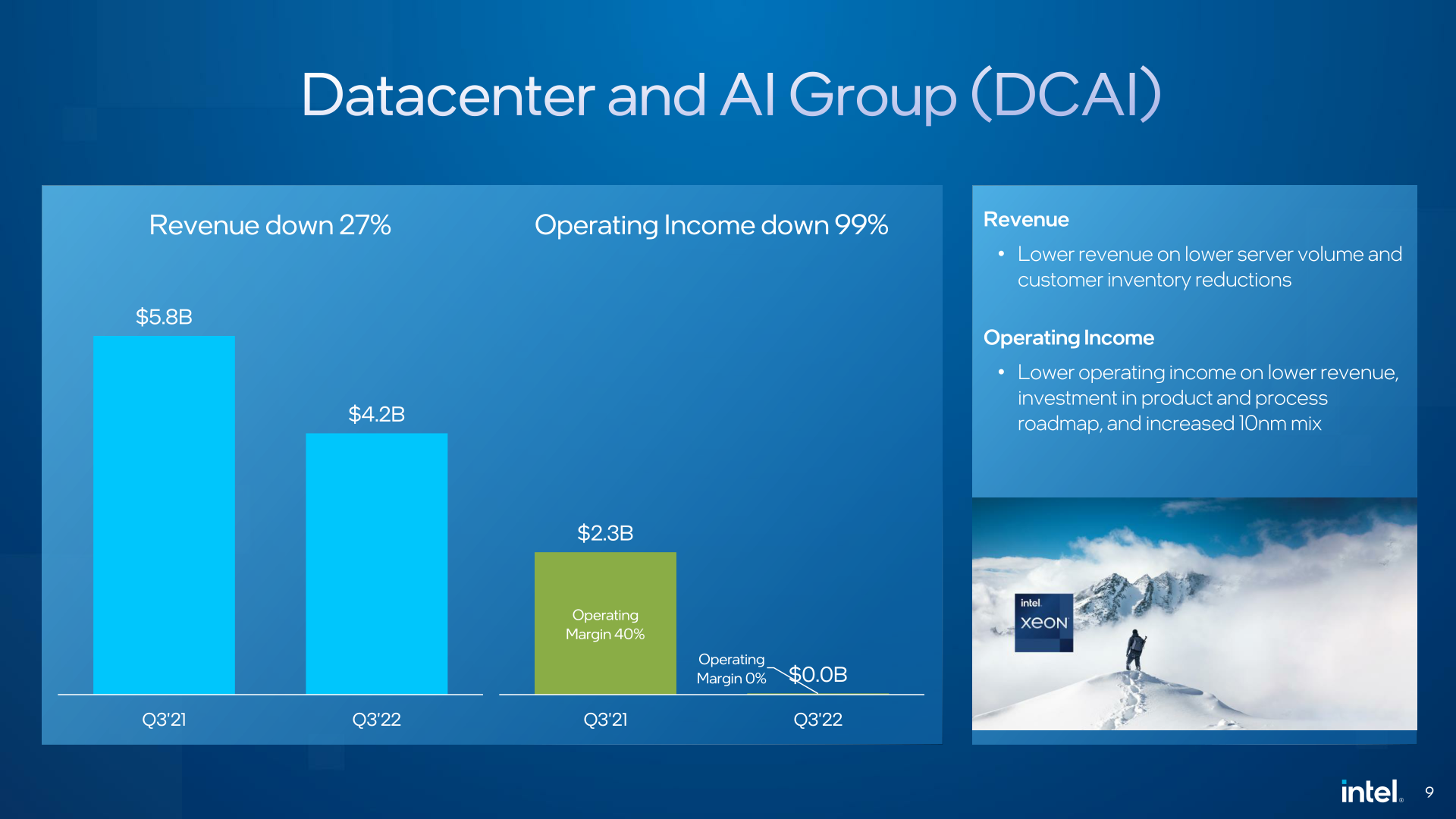

| Datacenter & AI Group Revenue | $4.2B | -9% | -27% | ||

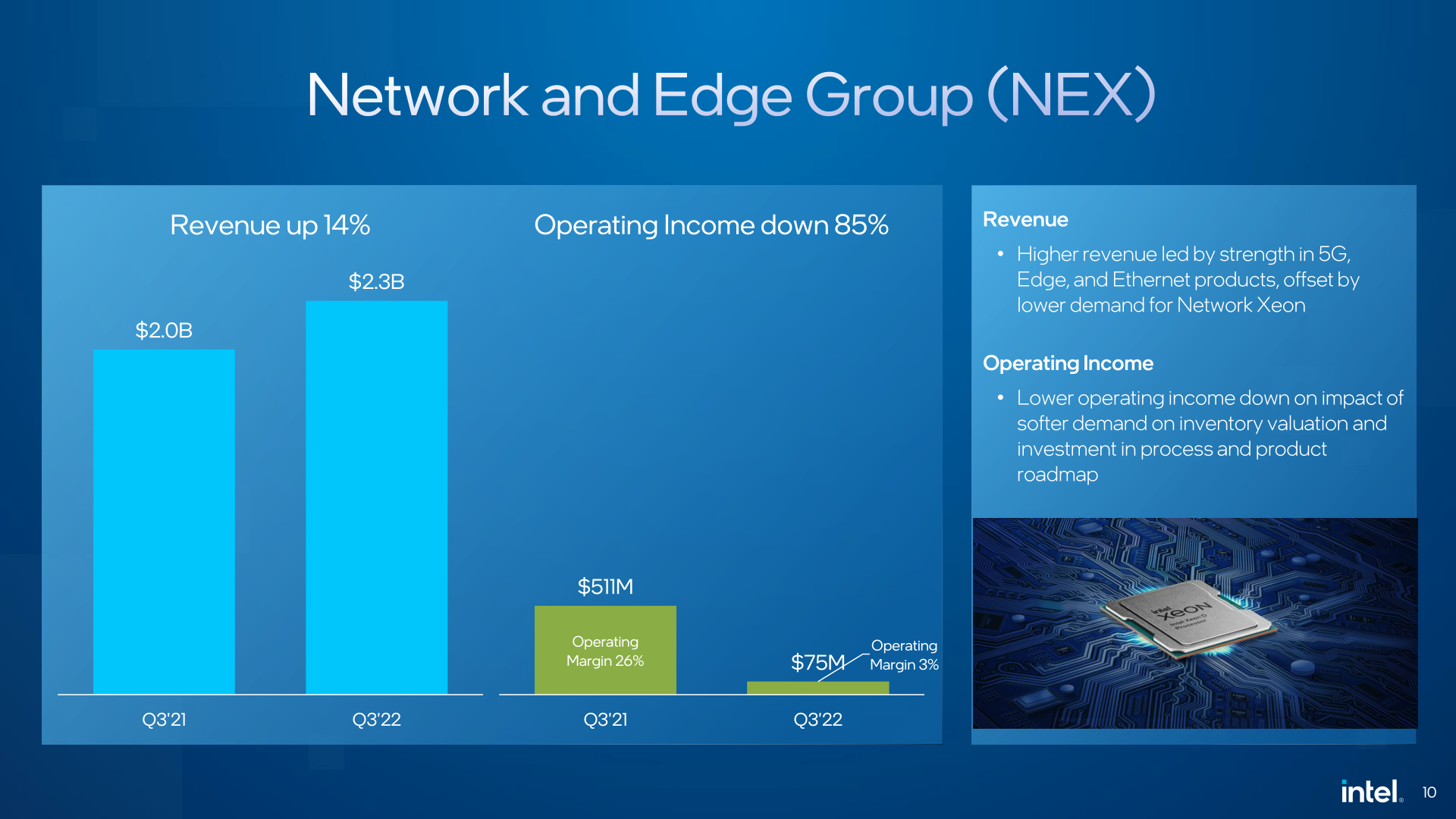

| Network & Edge Group Revenue | $2.3B | flat | +14% | ||

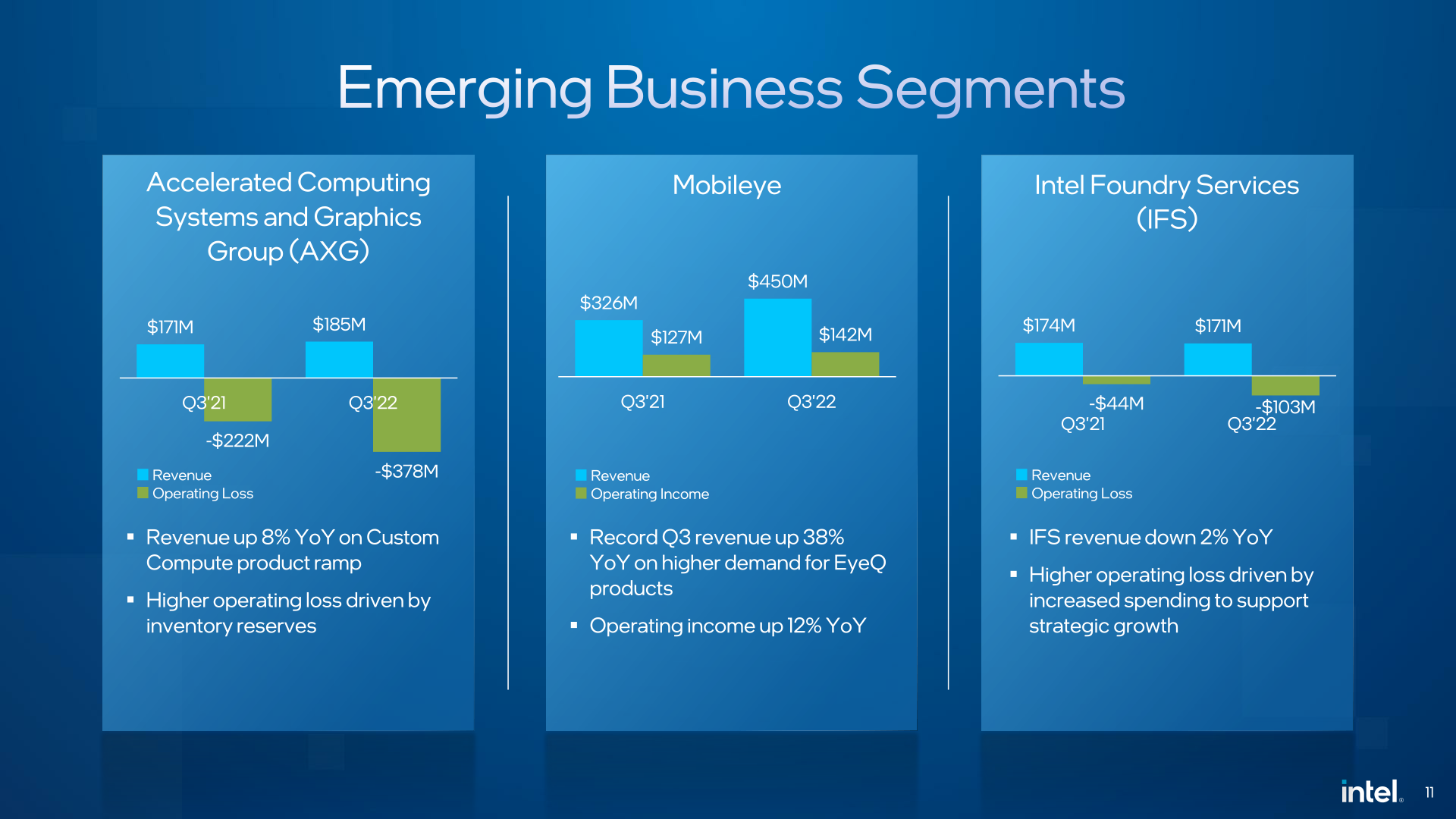

| Accelerated Computing Systems and Graphics Group Revenue | $185M | -1% | +8% | ||

| Mobileye | $450M | -2% | +38% | ||

| Intel Foundry Services Revenue | $171M | +40% | -2% | ||

With that said, after the hit Intel took in Q2, the company does appear to be turning the corner, if slowly. Gross margins have improved to 42.6%, which although still below Intel’s historical (or even recent) average, is at least high enough to keep the company’s operating income close to positive figures.

These figures also reflect some one-off charges, in particular a $664M restructuring charge that Intel is taking now in order to reduce ongoing costs (i.e. layoffs). We’ll go more into Intel’s future projections and actions a bit later on, but in short, while Intel is likely to have seen the worst of things on their end, Intel is once again reducing their revenue projections for the year as the bust cycle that the entire PC industry is going through isn’t over yet.

Breaking things down by Intel’s individual business groups, both of Intel’s major groups, CCG and DCAI, are down significantly on a year-over-year basis. Note that this is still the first year of Intel’s reorganized business groups, so Intel has needed to provide year-over-year comparisons for how the new groups would have performed if they were in place last year.

Starting as always with the CCG, Intel’s client group booked $8.1B in revenue, which is down 17% from the year-ago quarter. The most exposed to the collapse of the consumer market, CCG has been impacted by OEMs ordering fewer chips thanks to their own large inventories, as consumer and education system sales slow. Operating margins are also similarly down, due to a mix of lower revenues to book costs against and Intel’s continued investments in product development.

For the short term, Intel expects the Total Addressable Market (TAM) for the PC market to shrink by the “mid-to-high teens” for 2022, with that hit continuing through the rest of the year. The recent launch of Intel’s 13th generation Core (Raptor Lake) parts will help to induce some new demand, but not enough to fully offset the overall drop in the much larger PC market.

As for Intel’s Data Center and AI group (DCAI), the company took an even larger revenue hit there. For Q3 Intel booked $4.2B in DCAI revenue, down 27% from the year-ago quarter.

This drop in revenue has all but wiped out the operating profitability of the group, with Intel recording an operating income of $0.0B and an operating margin of 0% for the group. Intel is attributing the drop to lower sales of server/AI parts as customer demand weakens, while Intel’s relative costs go up as more and more server processors are shipped on the Intel 7 and 10ESF processes.

Intel of course is on the cusp of shipping its long-delayed 4th Generation Xeon Scalable (Sapphire Rapids) processors. So along with economic factors, customers are waiting for Intel’s next-generation hardware. According to the company, they officially shipped their “high-volume” Sapphire Rapids SKUs in Q3, though as the chips still haven’t made it as far as getting ARK entries, it’s clear that they’re not fully launched quite yet. None the less, Sapphire Rapids has reached PRQ (Product Release Qualification), which is the point where Intel is sufficiently happy that yields are high enough and the performance is suitable for silicon to be made for retail products.

Intel’s final billion-dollar business, the Network and Edge group (NEX) is the one real bright spot in this quarter’s earnings release. NEX revenue was up 14% year-over-year, reaching $2.3B.

Still, operating income was down severely, dropping 85% to just $75M for the quarter. Ultimately Intel saw strong demand for their more dedicated networking products such as 5G and Ethernet, while the Xeon products sold as part of this segment were hit with lower demand.

Finally, Intel’s “emerging” sub-billion-dollar groups were a mixed bag. AXG revenues are up slightly, but the group will continue to lose money for a couple of years to come until Intel has fully broken into the market and is shipping client and server GPUs in large volumes. Intel Foundry Services is in a similar boat, as Intel continues to make the investments needed to break into the contract fab market in a big way. Otherwise Mobileye was not only profitable, but grew year-over-year. Intel has just completed the Mobileye IPO this week, which although it is no longer a wholly-owned subsidiary of Intel, will still be a positive influence on Intel’s earnings sheet as Intel still owns most of the spin-off.

So what’s next for Intel from here? Even though the company believes they’ve already weathered what will be the worst of their quarters from a profitability standpoint, Intel still need to prepare both itself and investors for the rest of this bust cycle, and what’s (still) expected to be a general economic recession.

As far as Intel’s own projections go, the company is now calling for the 2022 fiscal year to deliver $63-$64B in revenue, which is down $2-$4B from their previous (Q2) projection. Which is to say that the market is going to be softer than what Intel was thinking at the end of Q2. If the new projections come to pass, this will put revenues for the year down 14%-16% from 2021.

This also means that Intel’s gross margin will not fully recover this year. The gross margin for the year is now projected to hit 47.5%, with Q4 in particular expected to hit 45%. Intel still expects to turn a profit, but with revenue for Q4 expected to decline up to 28% from the year-ago quarter, they’re not out of this yet.

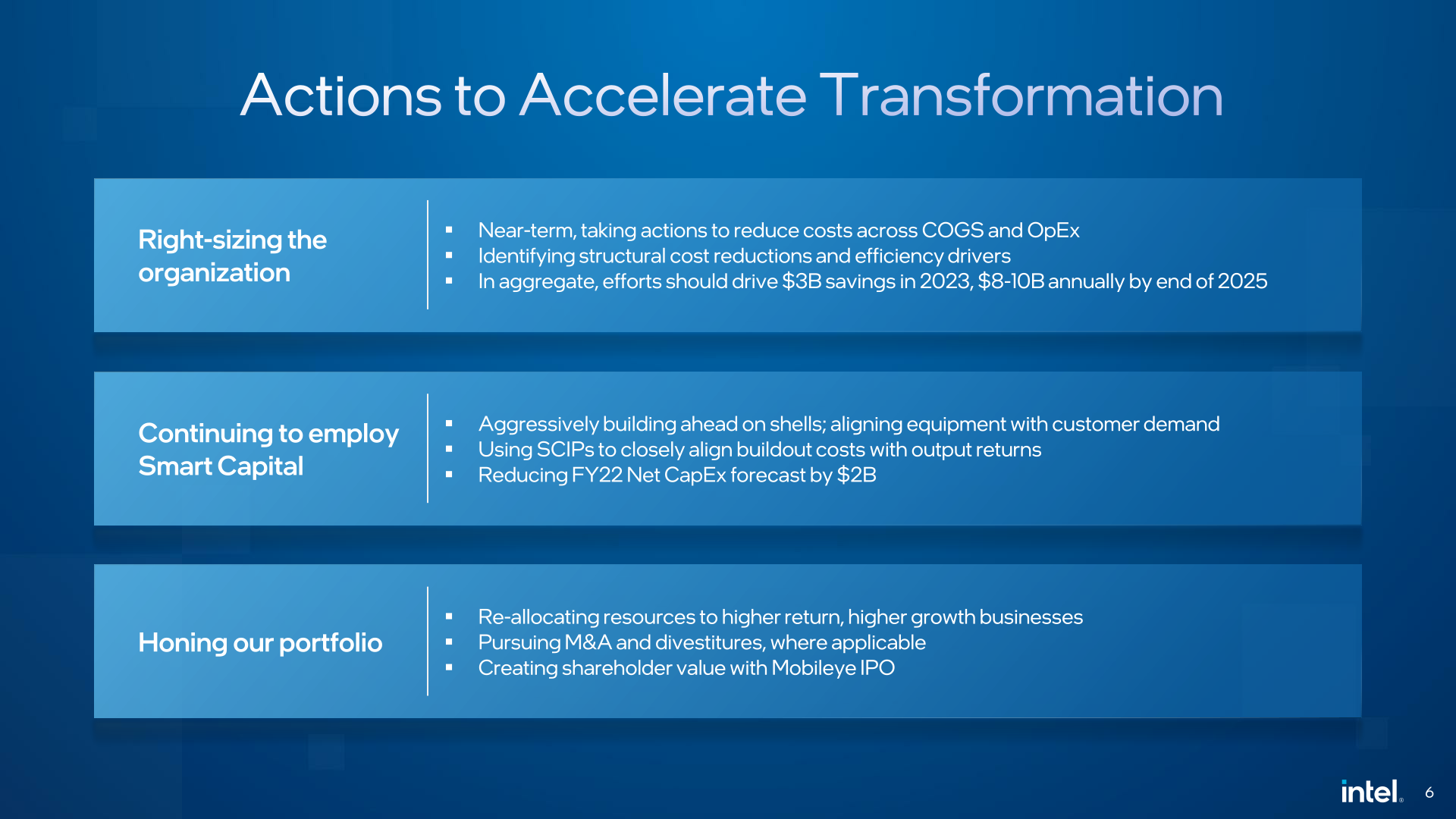

Given that Intel’s revenues and profitability aren’t expected to immediately recover, the company has made it clear that cost reductions, including layoffs, are on the way. Specific layoffs have not yet been announced (some of these will undoubtedly be announced in the coming days, now that the earnings period is over), but we know that Intel took a $664M restructuring charge in this quarter in order to enact those impending layoffs. At its current headcount, Intel has around 114,000 employees.

Altogether, Intel wants to save $3B in costs for 2023, with that accelerating into 2025. And as capital expenditures being one of Intel’s biggest costs, this is also where they will be making some of their bigger cuts. According to the company, they are going to continue building fab shells, and then fill them with equipment as demand dictates. This alone should allow the company to reduce capital expenditures by $2B for 2023.

Finally, Intel is also leaving the door open to any mergers, acquisitions, or divestitures that would benefit the company as it looks to focus on high-margin businesses. There is nothing specific here to announce today, but like any company undergoing belt-tightening, Intel is going to be looking at all of its options.

Overall, while Q3’22 has not brought Intel the same kind of beating as it took in Q2, the message from the company is that the challenges are far from over. As noted by CEO Pat Gelsinger in the company’s earnings release: “we are aggressively addressing costs and driving efficiencies across the business”, as Intel works to realign itself to ride out the rest of this bust cycle.

16 Comments

View All Comments

lemurbutton - Thursday, October 27, 2022 - link

Intel's Client and Computing group: -17%Mac sales: +25%

Apple Silicon shining through.

Samus - Friday, October 28, 2022 - link

You realize Intel sells more CPU's in a day than Apple sells Mac's in a year, right?shabby - Friday, October 28, 2022 - link

Don't hurt his feelingsWaltC - Friday, October 28, 2022 - link

Percentages are often misleading...;)name99 - Friday, October 28, 2022 - link

What you say may be true (though it seems unlikely to me, unless you start playing weird games with exactly how small a unit of a chip counts as a "CPU") but his overall point is valid.Compare Intel's Client revenue with Apple's WEARABLE'S revenue of $9.7B...

The point is not how Intel Client chips are so awesome and Apple wearables drool, or the reverse nonsense; the point is that the compute landscape changed irreversibly when Apple shipped the first iPod ~20 years ago, and Intel chose to fight that change (accept a new market that prioritized energy over EVERYTHING else, especially over caring about compatibility with the 1970s) rather than embrace it.

Intel had multiple fork points available (starting with owning StrongARM, then possibly switching to a new ISA and new design for Atom) and at every point they made the choice to prioritize the past over the future.

Now we are where we are today, and the trajectories aren't going to change. Intel will try to flee upmarket (as every company in its position does, cf IBM, cf DEC, cf SGI) and that will buy some time. But the MASS market has changed, and will change a lot more.

Simply screaming at this fact in fury won't change anything.

duvjones - Wednesday, November 2, 2022 - link

I think you misunderstand here, Intel's competition was never Apple. The guff you are making here about the consumer products is meaningless because, the cold truth is... Apple doesn't make semiconductors. The A series, the M series chips... Apple doesn't make them. It is not in the business of manufacturing. Taiwan Semiconductor Manufacturing Company is, and Apple is far from the only company in that arrangement of designing chip for someelse to make.Intel's target, it's real one, is to be on par with TSMC. A company that took over 30 years to be in this dominant position. Apple is irrelevant to that since they are beholden to whom ever can manufacture the chips and at the moment the manufacturers that can do it are only three of them.

Farfolomew - Monday, November 14, 2022 - link

I'm sorry, but Apple most certainly is one of Intel's main competitors. They are direct existential threat to Intel's main Intellectual Property: x86. Intel may be competing with TSMC on manufacturing, but they're also competing with Apple on architecture. Just like Microsoft may be competing with Google and Amazon on cloud services, but *also* Apple on personal computing platforms. Apple is just competing with everyone on everything, it seems LOL.Vitor - Saturday, October 29, 2022 - link

No. Intel cpu sales isnt 365 times larger than Apple Macs.lemurbutton - Sunday, October 30, 2022 - link

I would like to see the math.Blastdoor - Sunday, October 30, 2022 - link

Intel should do whatever it takes to get apple as a foundry customer. Start with the M-series and eventually go after the A-series. That would put Intel back on top.